Plug Power Ambitious Plans, Rising Solar PV Demand & Edotco

Plug Power Ambitious Plans, Rising Solar PV Demand & Edotco

1.) Plug Power Unveils Ambitious Plans

Plug Power’s share price rallied by 12% over the past 1 week.

Plug Power (PLUG), a leading maker of hydrogen fuel cells, is trying to rebound as momentum in renewable energy lifts shares. The company aims to produce more than half of its hydrogen energy from entirely renewable sources by 2024 and stands to benefit from a trilion-dollar infrastructure bill which includes $8 billion for hydrogen projects.

1H2021, Plug Power reported total revenue of USD196.5mn and net loss amounting to USD160.38mn.

The company incurred higher operating expenses as hydrogen prices remained highly elevated during 2Q21 due to supply shortages in North America.

The company also reported substantial costs associated with mobilizing their high-pressure tube trailers for their customers. Apart from that, Plug Power incurred Covid-19 related costs due to freight and material costs in the transit industry.

These costs will continue into the 2nd half of this year but should begin to abate if the global crisis subsides. Historically, Plug Power reported higher revenue during the second half of the year due to higher sales of GenDrive units. The company is expected to release its results in early November.

Oppenheimer analyst Colin Rusch raised the price target from $23 to $62 and reiterated a Buy rating. Rusch said, “While investors may be somewhat surprised by the capex associated with the build out of the hydrogen fuel business

Green Energy Plug Power To Invest $290M To Set Up Largest Hydrogen Plant In North America. Image Source: InvesBrain

2.) Xinyi Solar Holdings

Xinyi Solar’s (0968.HK) share price was up by around 11.97% from last week with the current price at HKD15.

Xinyi Solar Holdings Limited is an investment holding company principally engaged in the manufacturing and sale of solar glass. Along with subsidiaries, the Company operates its business through three segments. The Sales of Solar Glass segment is involved in the production and sale of solar glass products.

In 2016, the largest photovoltaic power station in the world was the 850 MW Longyangxia Dam Solar Park, in Gonghe County, Qinghai, China. In 2020, the base overnight cost of solar photovoltaic energy ranged from $1.248 to $1.612 per kW, which is significantly lower than the base overnight cost of conventional hydropower electricity of $2.769 per kW or geothermal one of $2.772 per kW. Image Source: IRENA

Key Trends & Insights

To provide a context of the solar panel market, it is expected to skyrocket and exceed $130B by 2030, driven by the increasing shift towards renewable energy worldwide. In 2020, more than 80% of all the world's newly commissioned electric power was from renewable sources, accounting for near 260 GW of the new capacity.

The company’s share price fell together with overall weaker performances of the renewable energy sector in China. So how fast is Xinyi Solar Holdings growing?

For starters, the company loses money each year, for long enough, investors still considering taking a loss on their share in the short run. The market is a voting machine in the short term, but a weighting machine in the long run. So let’s take a look at the company’s revenue and earnings growth trend with the following data:

Xinyi Solar is trading at LTM PE of 20.64x, which is cheaper compared to Flat Glass’ LTM PE at 24.59x.

Xinyi Solar’s PE in year 2019 and 2020 was 18.3x and 36.6x respectively.

The average selling price (ASP) of PV glass surged by 11.1% WoW to CNY30/m2 this week, most likely on rising costs of soda ash. Daiwa Capital expects the solar glass ASP to stay at a relatively high level on elevated module price, and to drop to more than CNY20/m2 over 1H22-2023, which is a comfortable solar glass ASP level for the top two players in the market, Xinyi Solar and Flat Glass, which would still earn a gross profit margin of more than 30%. Both Xinyi Solar and Flat Glass have around a combined market share of 60% - 70% in the world.

Source: SEHK:968 Earnings and Revenue History August 25th 2021

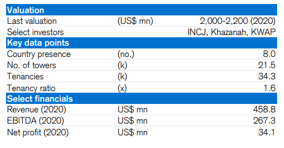

3.) Edotco Becomes the First Integrated Telco Infrastructure in Asia

Credit Suisse released a report titled ASEAN unicorns recently and included Edotco as one of the unicorns in this region. Edotco is one of the largest integrated telecommunication services company in Asia which specializes in end-to-end solutions in the tower services sector including co-locations, build-to-suit, energy, transmission, and operations, and maintenance.

The company has a presence across Asia in Bangladesh, Cambodia, Sri Lanka, Myanmar, Pakistan, Laos, and the Philippines.

As of June this year, the company has around 41,000 towers including 23,845 towers that are directly operated and another 17,860 towers under management.

Edotco offers tower sharing to multiple mobile network operators to reduce the overall cost of mobile operators. This helps to improve network coverage and lower the price for the customers. The need for towers is expected to increase as mobile operators expand 4G coverage and deploy 5G services.

Chart: Key Stats and Shareholdings of Edotco

Source: Axiata Annual Report